Shipping review of 2022 and what to expect in 2023

2022 was an eventful year – not just for the shipping industry. The UK’s Covid restrictions were lifted on 24 February, and on the same date, Russia invaded Ukraine, which has had a big impact on the world and on a lot of what is to come for 2023.

Trends from 2022

In shipping, Covid has impacted operations enormously. We have issues still with port congestion, delays and costing problems with maintenance and repairs, plus many crews became stranded on ships due to Covid zero-tolerance policies.

In Ukraine, because of Russia’s invasion, several ships became trapped in ports, some were damaged – and others sunk – in the Black Sea. The conflict has highlighted Europe’s dependence on Russia’s gas, but also on Ukraine’s grain. Trade of both has significantly dropped, descending the continent into an energy and inflation crisis. Prices of gas are at a record high, and oil is the highest price since 2008, presenting difficult challenges for shipping – not only in the cost of fuel.

Let’s not forget that Russia has been heavily sanctioned by the West. In the world of shipping, this meant the seizing of Russian Oligarchs’ superyachts, and many others became stuck in shipyards, halfway through repairs and construction, after Russian owners and investors were pulled from their involvement.

Shipping fuels

IMO 2020 Sulphur Cap – 3 years on

Initially, we foresaw some problems with the limitations set out in the IMO 2020 Sulphur Cap, however, three years on it appears not to have been the catastrophe we expected. The problems are there, but at a lower frequency than predicted.

One problematic example is from March 2022, when bunkered fuel in Singapore gathered more than 200 claims as a result of one supplier alone. Investigations found that High Sulphur Fuel Oil had been contaminated with organic chlorides. There was also High Total Sediment Potential (TSP) in Low Sulphur Fuel Oil (VLSFO) which had been improperly blended.

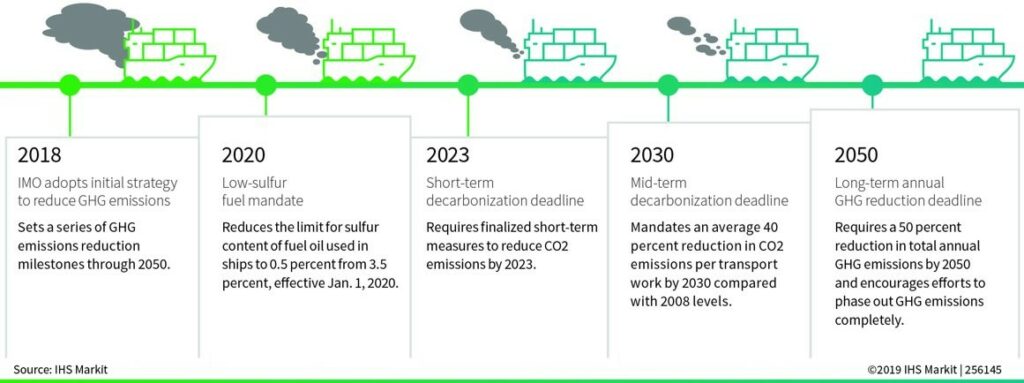

How will IMO 2050 be achieved?

We’re sailing towards zero-emissions shipping. “Decarbonisation” is the buzzword and will bring major change to shipping fuels in the next few years. Countries and industries across the world are committing to a major reduction in greenhouse gasses (GHG), and shipping is no exception. Current goals aim for -40% less CO2 from shipping by 2030, and -70% CO2 reduction by 2050. This will, in theory, reduce the industry’s total greenhouse gas emissions by 50% by 2050, when compared to 2008.

The shipping industry will reduce its carbon footprint, but how it is to reach these targets is the question.

Short term changes:

- Reduce fuel consumption

- More efficient vessel design

- Power limitation

- Propulsion aids

- Increase DWT

Long term changes:

- Replace carbon-based fuel (HFO & MGO)

- Alternative carbon-free fuel must be adopted (because LNG and Methanol are carbon-based)

- Hydrogen

- Ammonia

- Nuclear

- Battery power from renewable sources

Outlook for 2023

Going green

From 1 January 2023, it is now mandatory for all ships to calculate their Energy Efficiency Existing Ship Index (EEXI), to initiate and collect data for the reporting of their annual operational Carbon Intensity Indicator rating.

Ratings are on a scoring scale and based on the age of the ship and steps taken to improve the efficiency. Ships with consistently low efficiency ratings year-upon-year will have to take corrective action, enforced by administrations, port authorities and other stakeholders as appropriate.

What steps can shipowners take to improve their rating?

- Run on a low-carbon fuel

- Hull cleaning to reduce drag

- Speed and routing optimisation

- Installation of low energy light bulbs

- Installation of solar/wind auxiliary power for accommodation services

Alternative fuel uptake

Alternative fuels will see a huge rise in popularity over the next few decades as the drive to lower GHG emissions ramps up. Currently, 98.8% of ships in operation across the world’s fleet are running on conventional fuel supplies, but for ships on order we’re now seeing over 20% using alternatives such as hydrogen, methanol, battery/hybrid and LNG.

Ship operating costs inflation

It’s now more expensive than ever to repair vessels. Labour shortages post-pandemic are causing challenges with availability of technicians, resulting in costly delays, and the crews that are available come with higher wage bills, thanks to inflation.

All of this assumes that companies can find space in a dry dock to begin with. Repair yards are in high demand and over-subscribed, in part due to China’s Covid zero-tolerance policy. Spare parts are not readily available, and many are turning to manufacturers to plug gaps; the cost of lubrication oil has also surged by 15%.

All of which causes further delays to repairs, delays mean greater costs, and when operation costs are high, maintenance suffers.

Crewing crisis

The pandemic has created a seafarer shortage with many crews stuck onboard, unable to be repatriated, and leaving many to reconsider their careers. There is also a shortage of officers which is becoming critical.

Also important is that approximately 15% of global ship crews are Russian or Ukrainian, which is creating issues with dynamics onboard vessels. The impact has been considerable, for example if a Ukrainian crew members leaves ship to go home, they’ll be conscripted and unable to return to sea, leaving a potential 4% gap in global crew levels.

By Paul Hill

Enjoyed this overview? For full details of the year that’s passed and what’s to come, catch up on the briefing below:

You can see all our past Maritime Market briefings on our YouTube channel.

ABL Group offers independent energy and marine consultancy to the global renewables, maritime and oil and gas sectors. We combine expert knowledge with strong collaboration and insight, to deliver a fast, effective response to even the most urgent shipping challenge. We have a legacy spanning over 150 years in providing expert support to marine casualties of any type and size worldwide, from our offices located in 38 countries and all major maritime / shipping hubs.

Discover more about our maritime services: