The Gold Rush Continues – The New York Bight Leasing

ABL and OWC’s John MacAskill looks this week’s US offshore wind leasing in the context of the increasing valuations and competition.

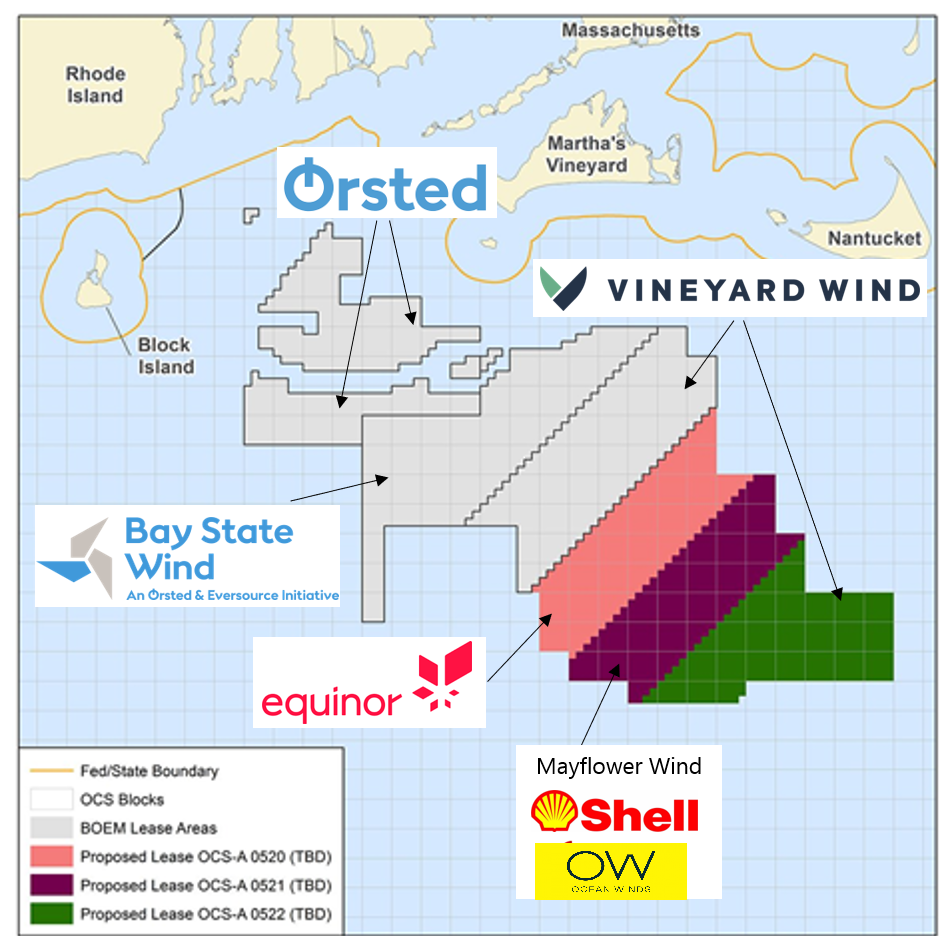

Back in January 2019 my colleague Juan Frias and I published two blogs covering the Massachusetts offshore wind lease that saw Equinor, Mayflower Wind (a joint venture between Shell and EDPR) and Vineyard Wind (a joint venture between Avangrid and CIP) part with a total record price of $405m (The Massachusetts Gold Rush – Part 1).

Stunning valuations

Since then we have seen evidence of stunning valuations as long participating Utilities and newer oil and gas entrants compete for offshore wind real estate in attractive markets. First Equinor, who paid $135m for Beacon Wind sold 50% of that project together with 50% of Empire Wind, a lease they had paid $42.5m in 2016, for a combined $1.1bn to BP. A stunning return for Equinor, but a necessary foothold in the US offshore wind market for an oil and gas major who is seriously looking to tilt towards being an ‘energy company’.

In the second part of the blog (The Massachusetts Gold Rush – Part 2), we also looked at this impact on future leases, in particular the UK’s Round 4. We stated that “since the UK offshore wind market is the safest short-term and long-term bet in Europe, we expect that the competition for these leases will be as fierce as it was in the Massachusetts auction.”

And so it was. The Crown Estate received option fees totalling £879m per year from the RWE Renewables, GIG/TotalEnergies, Floatation/Cobra and BP/EnBW., with the latter paying £462m alone. A number of factors were in play here.

Deep pockets

Firstly the demand. Mass’ 2018 and the England and Wales Round 4, where The Crown Estate only put 8GW of leases out for bidding, versus the 32GW in Round 3 over 10 years before, showed that there is a massive imbalance between the supply of leases and demand from developers. Governments and States are finding it challenging to screen and supply enough acreage to achieve the renewable energy and net-zero targets they set. This is due to conflicts with local stakeholders and the limited resources public bodies have to screen sites, structure, and launch selling processes.

Offshore wind lease crunch

Speaking to my colleague Juan Frias on this he told me, “So developers acknowledge there will be a route to market for the projects so the pace of offshore wind development is not slowed down. Governments need the projects built to achieve their renewable energy and net zero targets as much as developers to provide returns to their shareholders.”

Developers understand this supply crunch of available offshore wind real estate and this also comes with a great potential for future divestments. The potential to acquire large acreage enabling multi-gigawatt projects also enables portfolio effects and better procurement prospects also for other projects.

ScotWind, after a pause for breath, took a different road, and while still netting £699m in option fees from 17 projects totalling 25GW, as I stated in a January article, the specific ScotWind SCDS process, the delay/lag allowing the impact of Round 4 to be felt also drove an arms race for early supply chain development strategies and funds, with an expected c £800m-£1bn of commitments from the developers expected.

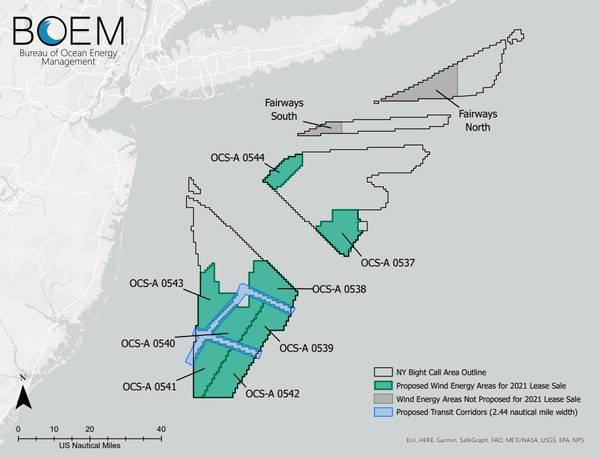

New York Bight

This is where we return to where I started, the East Coast of the US. Next Wednesday, the 23rd of February, we may learn the winners of 6 leases totalling up to 7GW of capacity, the most ever offered in the US in a single auction. Over 480,00 acres of prime offshore wind real estate in the New York Bight will be auctioned off, with the area’s 34-60m water depths, 8.5m/s wind speeds, and population/demand centres; I expect this lease to be heavily fought for.

It will be interesting viewing and I don’t expect this offshore wind bubble to burst anytime soon.

Watch out for upcoming OWC analysis of the outcome of this process.