Sustainability in Shipping: The Marine Fuel Dilemma

Trends in Sustainable Shipping

It is often quoted that shipping is 1.6 times less carbon emitting than a train, 10 times less than a truck or 47 times less than a plane, per cargo tonne, per mile. Those numbers might sound good, but if shipping were a country, shipping would be about sixth globally for carbon emissions based on 2015 data.

However, these statistics are eight years old, and shipping has improved since 2015, with more efficient vessels, tonnage replenishment technology, better hull cleaning, reduction in voyage speed, optimised routing, shoreside power and many other smaller initiatives to reduce emissions. The International Maritime Organization (IMO) even predicts that by 2025 all new ships will be 30% more energy efficient than those built in 2014.

So what is driving the significant change in energy efficiency of ships? New social and political pressures are pushing the shipping industry to reduce shipping-related emissions in a short period of time. Historically, energy efficiency in the shipping industry improved gradually and technology advanced slowly. This sudden increasing demand for a significant reduction will bring new challenges to the industry. Additionally, regulation is driving energy efficiency of shipping including initiatives such as the Cargo Owners for Zero Emission Vessels (members include Amazon Dupont, IKEA, Michelin, Target and Unilever) and the Energy Efficiency Existing Ship Index (EEXI) requirements, which are becoming mandatory from 1st January.

A Shift Towards Sustainable Options

Green Fuels

Although there are an increasing number of regulations pushing for energy efficiency, vessel owners have a number of choices moving forward, including which future fuel to select. Historically, the choice has been limited when changing shipping fuels: wind to coal, and coal to HFO. Now, fuel choices include HFO, LNG (Liquefied Natural Gas), Methanol, Electricity (Electric Battery), Hydrogen or Ammonia.

Shipping has, for the first time, key fuel decisions to make on a global scale. The DNV reports in its ‘Maritime Forecast to 2050’ that currently close to 99 percent of the world fleet is conventionally fuelled. However, 21 percent of vessels on order are non-conventionally fuelled.

Battery powered ships are typically near coastal operations that have frequent and regular port calls, such as northern European ferries or harbour tugs. In the use of batteries, these vessels are driven by Emission Control Areas (ECAs) that exist in various locations, such as parts of northern Europe.

Other options include LNG, methanol, hydrogen and ammonia. There are close to 1,500 LNG vessels, 813 battery or hybrid vessel, 46 methanol vessels and three hydrogen powered vessels on order or in operation globally; including from major owners such as Maersk, Stena Bulk, CMA CGM Berge and Hoegh Autoliners.

Hydrogen is widely produced – some 90 million tonnes per annum. Ammonia is also widely produced, with storage and piping well understood. Methanol is readily available at most global bunkering locations. Currently around 160 million tonnes per annum is produced. But notably, there is no surplus of these fuels today, so any increase in demand will need to be met with an increase in production. In the short term, the two may not align. Use of either Hydrogen or Ammonia is challenging at the moment, as there are technical and supply issues with both, as well as unresolved safety concerns with Ammonia.

Not all of these fuels are carbon free though. LNG is a carbon-based fuel and therefore can never be carbon free. Biofuels and e-methanol/bio-methanol are considered carbon neutral whereas ammonia and hydrogen are carbon free only if the energy source is from renewables – otherwise it is better, from a well to wake point of view, to use HFO. Electricity too can be carbon free, but, as with hydrogen, this depends on the source of the electricity. CH4 (which is the main component of LNG) could be carbon neutral alternative, but only if produced wholly with renewable energy and carbon captured, rather than through natural gas.

A vessel owner today must carefully consider the fuel type moving forward and factor in fuel availability, and impact on vessel design. The storage volume required may dictate which fuels are best for which vessels, for example, spare deck space for LNG tanks verses under-deck storage capacity for cargo. Hydrogen requires two and a half times, and LNG about one and a half times, more storage capacity than HFO. This presents a potential challenge moving forward.

Regulatory Framework

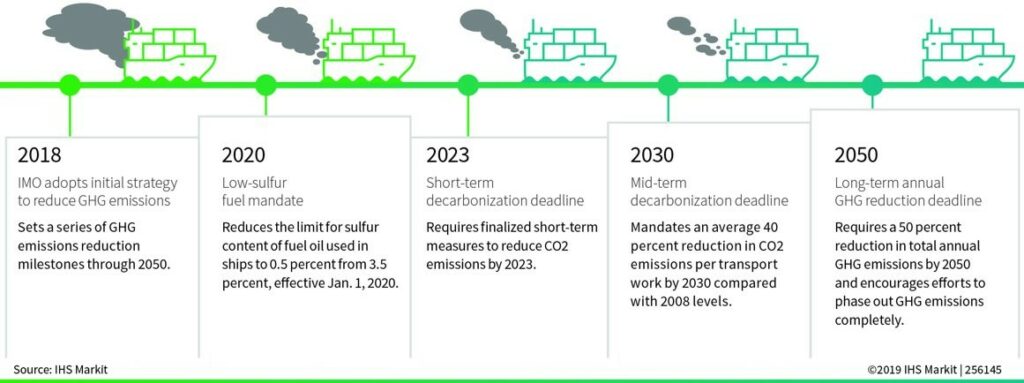

On top of vessel design challenges and potential supply chain gaps, shipping regulations are being put into place. For the most part, the IMO set global regulations to be followed, whereas now regulations are developing by region, adding complexity to the shipping scene. This may, of course, impact vessel owners’ ability to trade globally.

Ship owners are used to vessels being built to IMO conventions and class rules, as are insurers and charters. Now, catch-up is being played with regards to fast changing technologies and implementation of new marine fuels and systems.

In September 2021, the IMO Sub-Committee on Carriage of Cargoes and Containers finalised draft guidelines on safety for ships using fuel cells. This text was presented for adoption to the Maritime Safety Committee at a session in April of 2022. In parallel, the CCC sub-committee is also considering the development of guidelines for the use of ammonia and hydrogen as fuel.

One class society commented that it “responds to the latest understanding of safety for alternative fuel-powered fuel cells. But innovation is a continuous, dynamic process, and rules must be updated to reflect technical breakthroughs and feedback from real experiences”, and they are not alone in this journey. The same is valid for designers, builders, manufacturers of equipment and operators, as well as regulators.

There are limited standards to date, all case-by-case, which is less efficient and introduces risk to the owner during design and build.

The general view is that the IMO has been slow and cautious in imposing stricter decarbonisation targets. As a result, the industry is faced with impending regionalization of regulations as, for example, the EU pushes forward with stricter policies.

It is yet to be seen what impact the IMO’s Energy Efficiency Design Indexes will have on operations. There is possibility that there will be higher port fees for less efficient vessels, or these vessels will be banned from some geographic locations, or simply unwanted by some charterers. Equally could an “efficient” vessel today be reassessed in the future against a new benchmark making it unattractive long before its natural end of life? Could a new LNG-fuelled ship of today be unwanted in five years?

Conclusion

Change in the industry is needed but it needs to happen with safety and rules understood, crews trained, availability of fuels understood, and the cost impacts of change accepted by charters. However, it is complex, and the driver is society with urgent time frames. Ship owners today are having to make longer term bets in a changing market and the whole supply change needs to work together.

The ‘prisoner’s dilemma’ is often used to explain game theory, which in some respects the change from HFO could be modelled on this basis. The prisoner’s dilemma points to the best outcome for all ‘players’ and that is to cooperate and not to work in isolation. The shipping industry needs to in collaboration with each other to successfully move forward. ABL is here to help with managing the uncertainty.

ABL Group along with group company Longitude Engineering, have developed specialised in-house capabilities at pace with changing requirements in the market, to provide comprehensive advice and technical support to clients in their transition to more sustainable shipping solutions. Our services cover support from early advisory and feasibility, through to design and build, and subsequent marine and risk assurance. ABL Group is highly experienced in supporting with the detailed concept design, engineering, analysis and integration of clean shipping systems. Our services include:

- Design and engineering for clean shipping

- Electrical engineering for marine-based green technologies

- Ballast water systems engineering

- Exhaust gas emissions management

- Analysis and evaluation of viable vessel solutions

- Regulatory analysis